Did you know that small businesses are more likely to have financial constraints? For example, nearly 27 percent of businesses with 19 or fewer employees say they can’t take on more debt, while roughly 17 percent of those with 20-99 employees say the same, Made in Canada reports. Credit scores are a leading cause. Thankfully, factoring allows businesses to bypass the common hurdles of lending, but many still wonder about the factoring and credit link.

In this guide, we’ll explain how your credit score works, how it affects factoring, and how factoring can impact your credit score, empowering you to secure the funding you need while building stronger credit along the way.

Credit Scores 101: The Basics Explained

You’re probably familiar with some credit score fundamentals. If you manage credit wisely, your score goes up. If you manage it poorly or don’t ever use credit at all, you’ll have a lower score. That naturally has an impact when you apply for credit. Those with good scores are more likely to get approved and get better terms. Those with lower scores or challenged credit may not get approved and will typically pay more to borrow.

On the surface, this seems really simple, but there’s actually a lot more going on in the background, and being familiar with these nuances makes it easier to understand how factoring affects your credit score and vice versa. Let’s take a deeper look.

Credit Scores Come from Credit Bureaus

A credit bureau, also known as a credit reporting agency, collects information from those you do business with and then sells that information to creditors. The big bureaus here in Canada are Equifax, TransUnion, and Dun & Bradstreet (D&B).

You Have Multiple Credit Scores

People often talk about having a good or bad credit score. That can be a little misleading because you actually have lots of different credit scores. For instance, one of the most common personal credit scores is the FICO score. Around 90 percent of credit decisions are based on this score, and all credit bureaus can assign you a FICO score. However, because they may not receive the same data and there are many scoring models, each bureau may give you a different score.

As an alternative to FICO scores, credit bureaus may provide a VantageScore. While it works similarly, the factors considered and the way they’re weighted differ. Bureaus may also create industry-specific scores. For instance, some are tailored to auto loans, while others are related to credit cards. The list goes on.

Personal vs. Business Credit

It’s also important to note that you are likely to have both a personal credit score and a business credit score. Whereas Equifax and TransUnion tend to be the go-to for personal credit scores, D&B is more known for business dealings.

If you’re running a well-established corporation with a strong business credit score, there’s a good chance this is the only score a creditor will look at. However, your personal credit score may still be evaluated in these situations and becomes even more important as the size of a business, business credit score, and credit file of the business is reduced.

“Good Credit” Varies Based on the Model

It’s essentially up to a creditor which bureau they request a report from and which score gets used. To help provide some context, a few different models are outlined below.

FICO

FICO scores typically start at 300. Older FICO score models went up to 900. Newer ones stop at 850. A general breakdown of the ratings is provided below.

- Poor: 579 and below

- Fair: 580-669

- Good: 670-799

- Very Good: 740-799

- Exceptional: 800 and above

VantageScore 3.0

A VantageScore may be anywhere from 300 to 850, according to TransUnion.

- Very Poor: 300-600

- Poor: 601-660

- Fair: 661-720

- Good: 721-780

- Excellent:781-850

D&B

The most commonly used score in business is the D&B PAYDEX score. It rates businesses on a scale of one to 100 and uses risk categories to describe the ratings.

- High Risk of Late Payment: 0-49

- Moderate Risk of Late Payment: 50-79

- Low Risk of Late Payment: 80-100

The Factors that Impact Your Credit Scores Are Similar

Most credit scores use the same factors to rate you. They just differ in how much each one influences your score and the timeframes they use.

Personal Credit Score Factors

- Payment History: Whether you’re paying on time, have missed payments, or have public records, like a bankruptcy.

- Amounts Owed: How much credit you’ve used compared to what you have available. Less than 30 percent utilization is ideal, with the best scoring people being at ten percent or less.

- Credit Mix: Whether you have experience managing multiple forms of credit, such as installment loans and revolving credit.

- Length of History: Your oldest account, newest account, and average age of accounts.

- Recent Activity: New loans or hard inquiries that look more like you’re opening multiple lines of credit versus shopping for the best rates.

PAYDEX Score Factors

- Payment History: Paying on time will only get you a maximum score of 80. Pay early to boost your score even more.

- Trade Experiences: Refers to records of payment from suppliers, vendors, or other businesses you’ve paid. You need at least three to qualify for a PAYDEX score. More experiences, especially from a variety of businesses, boosts your score.

- Payment Amounts: Larger bills are weighed more heavily than smaller ones.

- Trends: Whether you’ve been consistent in paying on time, especially recently, your credit utilization and other details may impact your score.

Your Credit Scores Impact Many Aspects of Business

Maintaining strong credit is essential for lots of different reasons.

- Loan Approval: Each lender is different, but you’ll generally need a personal credit score of 650 or PAYDEX score of 75 to get approved for a loan.

- Interest Rates: The better your score, the lower your interest rate will typically be.

- Cost to Borrow: Picture two people applying for a $10,000 loan to be repaid over two years. The first has a credit score of 750 and qualifies for an APR of 7.87 percent. Their monthly payment is $244, and they pay $1,689 in interest over the course of the loan. The other person has a credit score of 650, so their APR lands at 11.96 percent. They wind up paying $263 a month and $2,632 over the course of the loan. Their monthly payment is about $19 higher, and they pay an extra $943 in interest.

- Credit Limits: Those with higher scores can generally secure larger loans and lines of credit.

- Insurance Premiums: From auto insurance to business premiums, those with lower scores typically pay more for insurance.

- Rental Agreements: Some landlords won’t rent to those with poor credit, while others charge more or require a larger deposit.

How Your Credit Score Impacts Factoring

Your credit score doesn’t play as big of a role in invoice factoring as it does with traditional loans or lines of credit. That’s because factoring companies are more interested in the creditworthiness of your clients. After all, they’re the ones responsible for paying the invoices. However, your credit score can still come into play under certain circumstances, and here’s how.

Factoring Focuses on Your Clients’ Credit, Not Yours

Factoring companies base their decisions primarily on your clients’ ability to pay invoices. If your customers have a solid track record of paying on time, it’s likely you’ll qualify for factoring regardless of your credit score.

There Are Still Times Your Credit Score Matters

Although the focus is on your clients’ credit, your personal or business credit score might come into play in certain situations.

- If Your Business is New: Without an established credit history for your company, a factoring company might assess your personal credit.

- If Your Financials Are Unstable: A history of financial mismanagement, like late payments or excessive debt, could lead to stricter terms.

- For Larger Advances: High advance requests, such as 90 percent of invoice value, may prompt a closer look at your credit to ensure you’re not overextending.

There Are Benefits to Having a Strong Credit Score When Factoring

While a great credit score isn’t necessary for factoring, having one can give you an edge. Here’s how it helps.

- Faster Approvals: Businesses with clean credit histories can breeze through the onboarding process.

- Better Rates: Factoring companies may offer lower discount rates to businesses they perceive as low risk.

- More Leverage in Negotiations: A strong credit history can boost your credibility and help you secure better terms

How Factoring Impacts Your Credit Score

While factoring isn’t a loan and doesn’t directly affect your credit score, your actions related to factoring can ripple through your financial health. Here’s a breakdown of how it works.

Timely Payments to Creditors Boost Your Credit Score

Factoring gives you quick access to cash by advancing funds against your invoices. This infusion of working capital can help you stay on top of your financial obligations, like paying suppliers, vendors, and creditors on time. Since timely payments are one of the most critical factors in determining both personal and business credit scores, factoring can indirectly boost your score.

Lower Credit Utilization Boosts Your Credit Score

By factoring invoices, you gain access to funds without increasing your debt load or credit utilization ratio. A lower credit utilization ratio (the percentage of your available credit you’re using) positively impacts your personal credit score.

Reduced Need for Credit Applications Boosts Your Credit Score

When cash flow is stable due to factoring, you won’t need to frequently apply for loans or lines of credit. Avoiding new credit applications prevents hard inquiries on your credit file, which could otherwise lower your score.

Failure to Meet Your Obligations Can Harm Your Credit Score

Your clients are responsible for paying their invoices. However, despite having strong credit management policies, there’s some chance that they might not. Whether or not this impacts you depends on the terms of your factoring agreement.

Recourse Factoring

Factoring agreements are typically categorized as recourse or non-recourse, with recourse agreements being the most common. Under a recourse agreement, if your client does not pay their invoice, you are responsible for ensuring the factoring company does not incur a loss. This usually involves buying back the unpaid invoice or providing another invoice of equal value to replace it.

Non-recourse agreements, on the other hand, shift the risk of non-payment to the factoring company. However, these agreements generally come with higher fees and may not cover all situations of non-payment. For example, non-recourse terms might only apply if the client’s non-payment is due to insolvency or bankruptcy, not other reasons like disputes over the goods or services provided.

If you fail to honour the terms of your recourse factoring agreement, such as repurchasing an unpaid invoice, the factoring company could report this to a credit bureau. This could potentially harm your business credit score.

Personal Guarantee

Some factoring companies require business owners to sign a personal guarantee. This means that, if a customer doesn’t pay, the business owner personally promises to cover the loss to protect the factoring company.

If you fail to fulfil a personal guarantee, such as by not repaying the factoring company when required, this default could be reported to a credit bureau. While not always the case, this could also impact your personal credit score, depending on the terms of the agreement and the factoring company’s reporting practices.

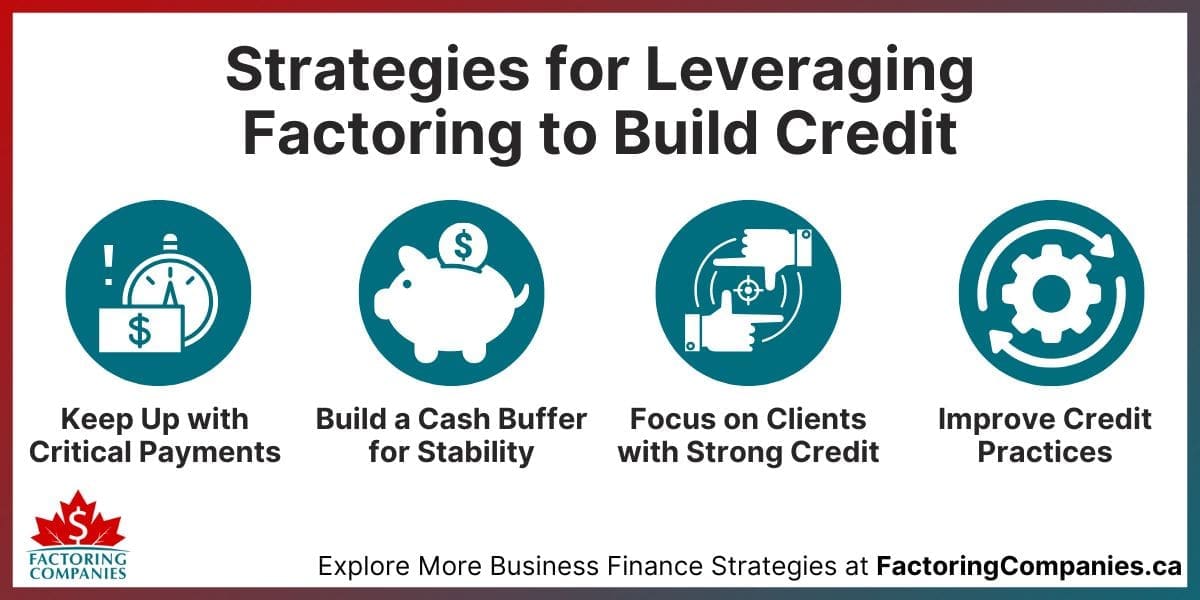

Strategies for Leveraging Factoring to Build Credit

Factoring can be a powerful tool for improving your financial health, but it works best when used strategically. It’s not a magic fix for underlying financial issues, but with the right approach, you can leverage factoring to build and maintain strong credit for your business.

Prioritize Critical Payments First

Use factored funds to pay high-priority obligations like suppliers, vendors, and fixed expenses. This ensures payments are made on time, boosts your PAYDEX score, and avoids penalties or disruptions.

Build a Cash Buffer for Stability

Allocate some of the liquidity gained from factoring to create a reserve for emergencies. A financial buffer reduces reliance on credit during tough times, which helps maintain a low credit utilization ratio and avoids additional hard inquiries on your credit file.

Focus on Clients with Strong Credit

Work with customers who have a solid payment history and creditworthiness. This reduces the risk of non-payment and ensures smoother approvals from your factoring company. Run credit checks or consult your factoring partner about potential clients when necessary.

Use Factoring as a Chance to Improve Credit Practices

- Create a Payment Schedule for Recurring Expenses: Organize your recurring payments to ensure creditors and vendors are paid on time.

- Develop a Strong Invoicing and Follow-Up Process: Streamline how you bill clients and ensure timely follow-ups on outstanding invoices.

- Set Up Reminders to Meet Your Obligations: Use tools or alerts to ensure you meet the terms of your factoring agreement consistently.

Get Fast Funding and Begin Building Your Business Credit Score with Factoring

Whether your business is credit-challenged and needs cash, wants funding without all the red tape loans have, or wants to boost its credit score through timely payments, lower utilizations, and fewer credit checks, invoice factoring can help. To take the first step, request a complimentary factoring quote.

FAQs About Factoring and Credit Scores

Can factoring help improve my credit score?

Yes, factoring can improve your credit score indirectly. It provides cash flow to pay bills on time, which positively impacts your payment history. Additionally, using factoring instead of credit lines reduces your credit utilization ratio, a key factor in your score.

What’s the difference between recourse and non-recourse factoring for credit scores?

In recourse factoring, you’re responsible for unpaid invoices, and failing to fulfill this obligation could impact your credit score. In non-recourse factoring, the factoring company assumes the risk of non-payment. However, higher fees and limited coverage (e.g., client insolvency only) are common with non-recourse agreements.

Do factoring companies check my personal credit score?

Some factoring companies may check your personal credit score, especially if your business is new or has no established credit history. However, their main focus is typically on your clients’ creditworthiness, as they’re the ones paying the invoices.

How can I use factoring to build my business credit?

Factoring helps build credit by ensuring consistent cash flow to pay suppliers and creditors on time. Prioritize payments that impact your PAYDEX score and maintain a transparent relationship with your factoring partner. Over time, strong financial practices supported by factoring can boost your credit.

Does invoice factoring appear on my credit report?

Factoring generally doesn’t appear on your credit report since it’s not a loan. However, if you default on obligations in a recourse agreement or fail to meet a personal guarantee, the factoring company may report it to a credit bureau, potentially impacting your score.

What happens if a client doesn’t pay their invoice in a factoring agreement?

If a client doesn’t pay under a recourse agreement, you’re responsible for buying back the invoice or providing another one of equal value. Failure to meet this obligation could harm your credit. Non-recourse agreements shift this risk to the factoring company, but the terms are stricter.

Do I need good credit to qualify for factoring?

No, factoring focuses more on your clients’ creditworthiness than your own. While poor credit may affect your terms—such as higher fees or personal guarantees—you can still qualify for factoring if your clients have strong payment histories.

Can factoring reduce my credit utilization ratio?

Yes, factoring can reduce your credit utilization ratio. By using factored funds instead of maxing out credit lines, you free up your available credit. A lower utilization ratio is beneficial for both personal and business credit scores.

About Factoring Companies Canada

Get an instant factoring estimate

Factoring results estimation is based on the total dollar value of your invoices.

The actual rates may differ.

CLAIM YOUR FREE FACTORING QUOTE TODAY!

PREFER TO TALK?

You can reach us at

1-866-477-1778

Get an instant factoring estimate

Factoring results estimation is based on the total dollar value of your invoices.

The actual rates may differ.

CLAIM YOUR FREE FACTORING QUOTE TODAY!

PREFER TO TALK? You can reach us at 1-866-477-1778